Bangkok Cost of Living 2026, Part 1: Why It Costs More Than Taipei

A comfortable month in Bangkok costs ~$1,600 in 2026 — more than Taipei, despite the "cheap Southeast Asia" reflex. The full line-by-line breakdown. Part 1 of 2.

Here's the finding that surprised me most, and it's the one this post is built around: a comfortable single remote worker in Bangkok in 2026 lands around US$1,600/month, and that's above Taipei's comfortable budget (≈$1,175), not below it. "Cheap Southeast Asia is pricier than East Asia" is a sentence that shouldn't be true, and it's the kind of thing you only catch by pricing two cities the same careful way and laying them side by side. The reflex that Southeast Asia is the budget option doesn't survive a line-by-line look, and in Bangkok's case it's wrong by more than $400 a month. (Da Nang, the third city in this series, stays the genuine cheap base; it's Bangkok-vs-Taipei specifically that flips.)

I’ve spent time in Bangkok recently enough that I trust myself on the shape of the city — how Sukhumvit reads at street level versus from a skywalk, why Asoke at 6pm is its own small ecology, the difference between a soi in Ari and a soi off Thong Lo. What I do not trust myself on, from memory, is what any of it costs in 2026. The condo market here moves enough quarter-to-quarter that pricing from a year-old impression is its own form of guessing. So I priced this the same way I priced Da Nang: from current listings on the platforms residents use, in their language, cross-checked against the English-language foreigner-facing sites to size the gap.

This is the paid layer, and it’s the first half of a two-part Bangkok teardown. Part 1 (this post) is the cost layer: the area-level math underneath that number, the two decisions that move your Bangkok rent more than any neighborhood choice (neither of which is what English Bangkok guides will tell you), the daily-living and grocery math, and first in this series, a three-way comparison against Da Nang and Taipei, line by line. Part 2, this Saturday, is the decision layer: healthcare, the restaurants residents actually use, the visa landscape after the 2024 DTV launch (which genuinely rewrote the playbook for remote workers), and the honest verdict on who should choose Bangkok over the other two. Bangkok ran long enough to deserve both halves done properly rather than one rushed pass.

Orientation — is Bangkok even for you?

(Already set on Bangkok and just here for the numbers? Skip to the methodology below.)

Here’s the honest case, before the spreadsheet, and it isn’t the brochure’s. The draw is not that Bangkok is cheap; the whole finding of this post is that it isn’t. The draw is that it’s a fully-functioning major Asian capital where a remote worker on a non-Thai income gets a rare bundle: world-class private healthcare you can pay cash for, genuinely world-class food at every price tier, a city built around trains so you never need a car, and — for the first time in a decade — the easiest legal-residency landscape of any big Asian capital (the 2024 DTV; full menu in Part 2). That combination is the reason to come. The low price is not.

The trade-offs are just as real. It’s not the budget option — Da Nang is, and this post shows by exactly how much Bangkok isn’t. The 180-day tax-residency clock is a real trap the easy visa doesn’t solve (Part 2). And the climate is its own cost: relentless heat, a genuine bad-air season, and traffic among the world’s worst — workable only because the trains are good and you plan your life around them.

Who thrives here: a remote worker earning in a stronger currency who wants a big-city base with great food, deep healthcare, and an easy visa, and isn’t trying to grind the rent to the floor. Who should look elsewhere: anyone chasing “cheapest Southeast Asia” (that’s Da Nang, or at most Bangkok’s far-east-Sukhumvit floor), anyone who needs to live on a Thai salary, and anyone who wilts in heat or wants a walk-everywhere rather than a train-everywhere city.

A note on currency: ≈32.5 THB = US$1 .THB figures are written as 25,000 THB (≈$769) throughout.

1. The methodology (and why it matters)

The dominant English-language source for Bangkok cost-of-living is a mix of Numbeo aggregation, foreigner-targeted condo-rental sites (Hipflat in English, DDproperty in English), and a cohort of 2021–2023 “moving to Bangkok” blogs that predate the current visa landscape. For Bangkok in 2026, all three are misleading, in a more subtle way than Da Nang’s foreigner channel was. The English Bangkok internet doesn’t quote you a flat 2× markup. It does two quieter things: it shows you the wrong geographic resolution, and it shows you the wrong half of the inventory. Stacked, those two omissions are most of the “Bangkok costs $2,000+/month for a foreigner” assumption.

Here’s what I did instead:

Rent data — the Thai-channel baseline: pulled live from DDproperty Thailand in Thai (ddproperty.com/th) and Hipflat TH (hipflat.co.th). The Thai-language interface surfaces stock the English one filters out, and tags each listing with a server-computed walk-time to the nearest BTS/MRT exit — the detail this whole analysis turns on. n=84 listings across six station clusters (Asoke, Phrom Phong, Ari, On Nut, Huai Khwang, + partial Phaya Thai), after excluding the stock that distorts a median: tourist-priced short-stays, ultra-luxury branded residences, unfurnished shells, mislabeled whole-house leases.

Rent data — the English foreigner-channel comparison: a parallel sample on Hipflat EN (hipflat.com), which searches by Bangkok administrative district rather than by station, a resolution mismatch that turns out to be the whole story of §2.

Utilities: electricity against the MEA (Metropolitan Electricity Authority) published residential tariff, including the June 2026 restructure (worked calc in §5); water against MWA; internet against AIS Fibre / True Online; mobile against AIS / True / DTAC.

Groceries: online-catalogue list prices across four Bangkok chains — Lotus’s and Big C (mass-market), Tops (mid-tier), Gourmet Market (premium) — priced per-unit on a Thai cook-at-home basket and a Western-imports basket.

Healthcare, visa, tax, and restaurants are covered in Part 2 — the decision layer.

Every figure below traces to a specific source. Where I’m uncertain — or where the data has a genuine limit — I flag it.

The advantage here is bilingual sourcing, and in Bangkok it pays off in a specific structural way. The English-language rental internet and the Thai-language rental platforms don’t just describe two prices for the same flat. They describe the same Bangkok at two different resolutions: the English channel aggregates to Bangkok administrative district (Watthana, Phaya Thai), the Thai channel aggregates to BTS/MRT station. For 95% of resident decisions, the station is the address — and the district average buries the station premium. This post does the cross-walk so you can see what a resident sees, not what the English district average tells you.

2. The two decisions that move your rent more than the neighborhood

Two questions move your Bangkok rent more than any neighborhood choice, but neither one is what English Bangkok guides will tell you. They’re the channel you search and the resolution you search at; and which specific station you anchor at, with what kind of stock that station has.

Decision 1: Which channel — and at what resolution

The English Bangkok rental sites (Hipflat EN, DDproperty EN, JustProperty) do two things differently from the Thai-language platforms (DDproperty TH, Hipflat TH). They show you condos rather than the older single-owner stock, and they search by Bangkok administrative district rather than by BTS station.

The first difference matters less than I’d assumed before the data. The Thai-platform อพาร์ทเมนต์ (apartment) category, on close inspection, isn’t a cheaper version of the condo product — it’s a different product: older, larger (75–500 m², mostly 2–3BR), foreigner-family-oriented privately-held towers at ฿55–250k/month. Same square meterage in the apartment category routinely costs more than in the condo category. The genuinely-cheap walk-up rental tier that Bangkok tenant lore describes — the resident-Thai working-class stock at ฿5–10k for a 30 m² unit — exists, but it doesn’t index on DDproperty or Hipflat. To find it you’d need Facebook Marketplace housing groups, LINE-based agent networks, or physical “ห้องเช่า” (room for rent) signage walks. None of those surface in either the foreigner or the major Thai-language platforms. For this post, the rental analysis is condo-vs-condo across channels — which turns out to be where the more interesting moat lives anyway.

The second difference is the real one. At one station, the foreigner channel quotes a clean premium over the Thai-channel station median. At another, it appears cheaper, but only because it’s hiding the premium station inside a district-wide average.

Here’s the picture at Huai Khwang (MRT Blue Line, BL18), where Hipflat EN’s “huai-khwang” district slug aligns reasonably tightly with the actual BL18 station catchment, the Thai-channel 1-BR median runs ฿21,000 (≈$646) vs the foreigner channel’s ฿24,228 (≈$745) — a clean +15% — and the 2-BR ฿31,000 vs ฿39,096, +26%.

That’s the cleanest channel-premium picture across all six clusters, and it’s what Thai-speaking residents on local-language platforms independently flag as the foreigner-channel markup in Bangkok: real, but in the 15–30% range, not 2×.

Now the same picture at Phrom Phong (BTS E5), the premium Sukhumvit station where Hipflat EN’s foreigner-channel search uses the “Watthana” district — which spans six BTS stations east, all the way out to Phra Khanong — the foreigner channel quotes ฿27,540 (≈$847) for that district average, 47% below the Thai-platform Phrom Phong-station median of ฿52,000 (≈$1,600).

That inversion makes no sense at first read. It is not real. The Watthana district median averages in cheaper Ekkamai and Phra Khanong condo stock 2–6 stations east of Phrom Phong. The foreigner channel isn’t pricing Phrom Phong-the-station; it’s hiding Phrom Phong-the-station inside a district average. You think you’re paying ฿27,540 for “premium Sukhumvit” and you are, but not for Phrom Phong specifically. The Phrom Phong-station rent on the Thai platform is ฿52,000, and you’ll find that out when you actually go look at the building.

So the channel-premium isn’t a Bangkok-wide tax. It’s: real and ≈15–26% when the foreigner channel’s district geography happens to align with a station catchment, and structurally invisible-or-misleading when it doesn’t. The English Bangkok internet is showing you the right city at the wrong resolution. Knowing the difference between the two — and knowing which question you can ask the Thai channel that the English channel will quietly answer wrong — is the moat.

Decision 2: Which station — and what stock that station has

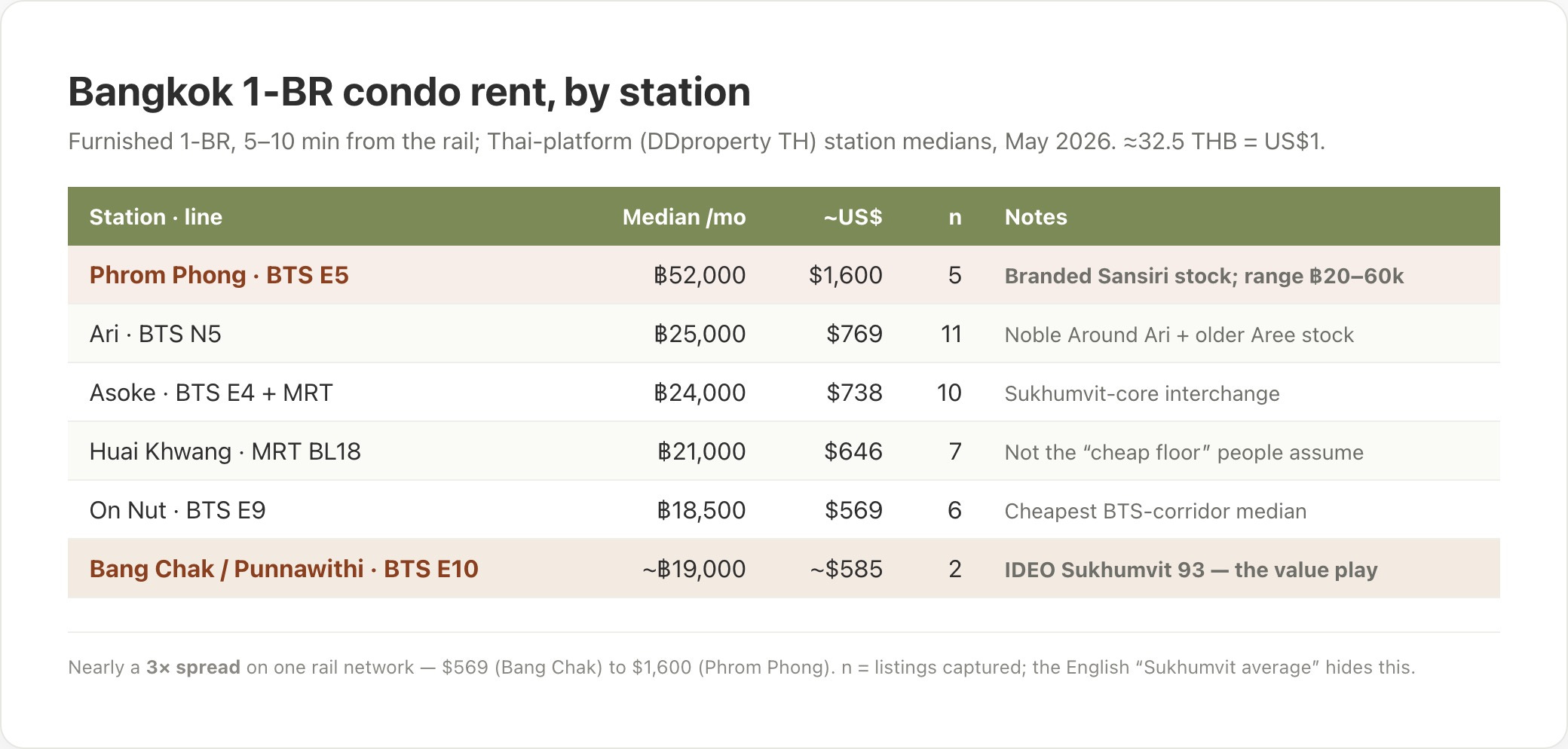

Here are the Thai-channel medians for a furnished 1-BR condo, across the six BTS/MRT clusters where local renters actually shop:

Almost a 3× spread across the same Bangkok rail network. The headline: same kind of unit (furnished 1-BR condo, 5-10 minutes from a rail station), and your monthly rent goes from $569 to $1,600 depending on which station you anchor at. None of the English Bangkok guides give you that picture station-by-station; they give you a “Sukhumvit costs $X” district average that’s not the price of any specific flat you can actually rent.

Three things that picture says, and the English Bangkok content doesn’t.

First — the “MRT cheap floor” reputation is wrong. Every English Bangkok guide describes Huai Khwang and the MRT Blue Line as the genuine cheap floor near the center, on the logic that MRT-only is less expat-coded than the BTS Sukhumvit corridor. The Thai-channel data says no. Huai Khwang 1-BR at ฿21,000 is only ≈12% below Asoke ฿24,000, and it’s above On Nut ฿18,500. The MRT-vs-BTS distinction isn’t the price driver in Bangkok. Station-specific anchoring is. The genuine cheap floor on the rail network is east of On Nut, on the BTS Sukhumvit line — not on the MRT.

Second — Bang Chak and Punnawithi are the genuine BTS-corridor value play, not On Nut proper. On Nut at ฿18,500 1-BR is cheaper than Asoke, but it’s not the floor. One station east at Bang Chak (BTS E10), IDEO Sukhumvit 93 lists 1-BR units at 35 m² for ฿19,000 and 2-BR at 54 m² for ฿29,000 — roughly 35–40% cheaper than the same-spec product one station west. Two stops further east from the foreigner-default Asoke buys you 60%+ off rent for the same train. The “value still on the BTS Sukhumvit corridor” point is real and quantifiable: it’s specifically Bang Chak/Punnawithi, not On Nut.

Third — at non-foreigner-dense neighborhoods, the BTS-proximity premium decays into a building-age premium. In Ari the brand-new Noble Around Ari (2023 build, 2-minute walk from N5, 26–45 m² units) and the older Fynn Aree / Vertical Aree / Noble ReD stock (2009–2017 builds, 4–10-minute walks) all sit in the same ฿17–30k 1-BR band. You’re not paying for proximity at Ari; you’re paying for newness. The close-to-BTS premium only really bites in the Sukhumvit core (Asoke, Phrom Phong, Thong Lo) where close-to-station stock IS branded ultra-premium product. Outside that core, the close-stock advantage is small or zero.

The practical takeaway: the right two questions in Bangkok aren’t “what neighborhood?” and “what budget?” They’re “which channel and at what resolution?” and “which station anchors my actual life?” Get the first one right and you stop paying invisible aggregation premiums. Get the second one right and you stop paying $330–780/month for “I want to live in Sukhumvit” when what you actually need is “I want a BTS-connected flat with a 7-Eleven downstairs,” which Bang Chak provides at a third of the Phrom Phong price.